Europe’s Smelters: The Strategic Assets We Cannot Afford to Lose

Op-Ed by Richard Holtum, CEO of Trafigura

Richard Holtum, CEO of Trafigura, will deliver the keynote and open the EIT RawMaterials Summit 2026 on 20 May in Brussels.

The conflict in Iran highlights a now-familiar pattern: geopolitical shocks disrupt supply, prices spike, and European industry pays the price. The Russian gas crisis offered hard lessons. The question is whether Europe has learnt them.

Energy is not Europe’s only strategic vulnerability. Critical metals processing is next. The assumption that global markets will reliably deliver essential industrial inputs has left Europe’s smelting base in decline — and the consequences are becoming clear.

This is not a niche issue. Metals processing underpins every major industrial sector —defence, automotive, construction, electronics. Zinc, copper, lead and aluminium are the foundation of European industry. More critically still, smelters produce the by-products essential for defence and high technology applications: without lead smelters there is no antimony; and without antimony, no bullets.

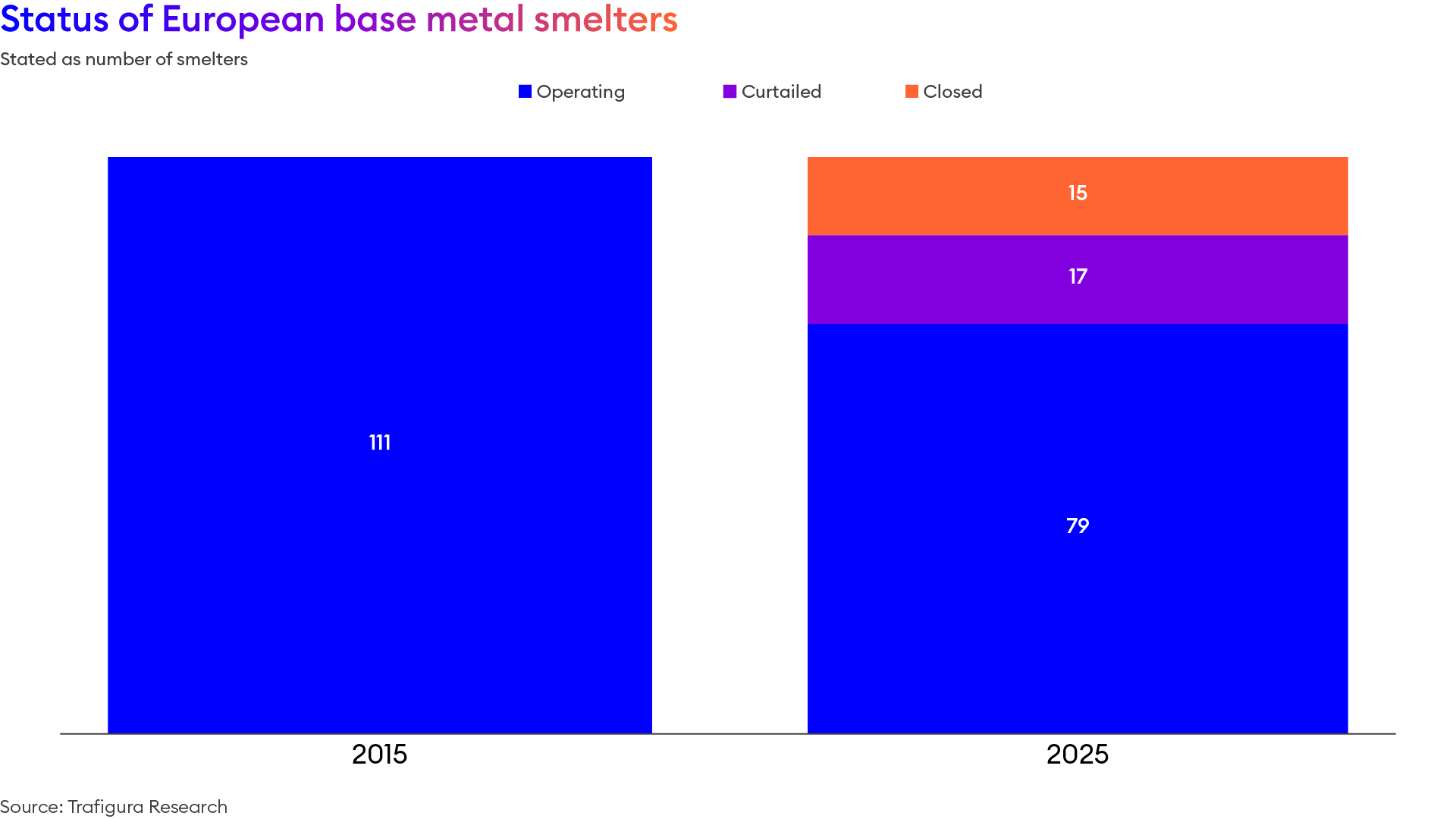

Over the past decade, nearly a third of Europe’s base metal smelting capacity has been closed or curtailed. Structural factors — high energy and labour costs, weak refining margins, and competition from state-backed or subsidised producers — have made much of the sector uneconomic.

Europe has also failed to capture the full value of the critical minerals its smelters already produce, ceding ground by default to China.

The good news? Europe retains a significant industrial base of metals smelters. It remains broadly self-sufficient in midstream processing — an advantage that would take decades and billions to rebuild.

With targeted investment, existing assets could be modernised and expanded. The expertise is still here — for now.

The challenge is that markets alone will not solve this. The private sector cannot fully price national security, industrial resilience, or the strategic value of supply chains. Projects that are strategically essential often appear commercially marginal. This is precisely where public policy must step in.

Aerial view of the Nyrstar Balen smelting facility in Belgium, operated in partnership with Trafigura—a key industrial site for zinc processing within Europe’s critical raw materials value chain.

Three priorities stand out.

First, protect what exists

European smelters face structural disadvantages. Energy can account for up to 60% of production costs, yet prices are set globally and cannot be passed through. At the same time, inconsistent grid tariffs and compensation mechanisms distort competition within Europe itself. Reforming grid tariffs, extending compensation for indirect ETS costs, and adopting a coherent approach to energy support are essential to prevent further closures.

Second, create a viable business case for critical minerals

Smelters can supply materials such as germanium and antimony, but doing so requires additional processing investment. At Nyrstar, adding germanium recovery capability would cost around €100 million per site — modest relative to its strategic value. Yet volatile prices and cheaper subsidised supply undermine commercial viability. Targeted tools — long-term offtake agreements, price floors, and public co-investment — are needed to unlock these projects.

Third, invest to modernise and fully utilise existing assets

Smelters can also support the energy system. Electrified plants can adjust production to balance intermittent – and growing - renewable supply. But this flexibility requires investment and market frameworks that reward, rather than penalise, it. With the right support, smelters can strengthen both industrial resilience and energy system stability.

Other nations, notably the United States, are deploying capital and policy support to rebuild capacity that has already been lost. Europe, however, still has the assets, skills and opportunity to lead — not only in securing domestic supply, but in providing processing capacity for allied economies. But time is limited. Smelters do not simply restart once closed: equipment degrades, workforces disperse, and expertise is lost.

Europe must move quickly to secure these strategic assets before they are irreversibly lost.